By Raul Elizalde

This article also appeared on forbes.com

In 1955, the then-chairman of the U.S. Federal Reserve, William McChesney Martin, explained that one of the functions of the Fed was to order “the punch bowl removed just when the party is really warming up.” Jay Powell, the current chairman, has taken that teaching to heart. After saying a couple of weeks ago that the time has come to stop calling inflation “transitory”, he followed up with the announcement that the Fed will reduce money injections via bond purchases much faster than planned. The market thinks that it will end all purchases by next March, at which time the Fed will also start hiking rates. At the moment, the consensus is that it will do so three times before the end of 2022.

A stingier Fed is not something that the market usually likes, but the highest inflation readings in decades leaves the central bank with little choice, if nothing else because it needs to show that it is doing its job. It is far from evident, however, that higher rates would have any impact on taming inflation if the reason why prices are climbing is because of the well-known crunch in global supply lines.

No amount of Fed tightening will clear waiting ships, production stoppages in Southeast Asia or a shortage of truck drivers, unless it raises rates so far beyond the forecasts and depresses demand so much that shortages won’t matter anymore. This is not impossible: the market is aware that the Fed has overdone past tightening bouts and could do so again.

Rates and inflation are only a partial list of worries. Omicron, the new Covid-19 variant, is also weighing on sentiment as it sparks a new round of preventative restrictions in Europe and the U.K. that could impact their economic recovery. The variant is also spreading rapidly in the U.S., just when some economic indicators such as regional activity indices or retail sales show signs of cooling down. Nobody really knows how the ever-changing, never-ending pandemic could affect conditions in the months ahead, which is bad news for a market that places a high value on certainty.

Does this all mean that the decade-plus bull market is over? The optimistic view is that the labor market remains strong, the consumer is still in good shape and companies have maintained healthy profits despite supply chain disruptions. Early indications here and there that these may be easing have led some to think that once resolved, the pendulum will swing to an excess of supply caused by ramped-up production and inflation will come down very quickly. Given how the pandemic has confounded all forecasts, this is as plausible as anything else.

Market dynamics, however, point to a deteriorating outlook for stocks. First, volatility indices in the Nasdaq 100 and the S&P 500 spiked in early December and remain unsettled. The volatility indices reflects the cost of insuring a portfolio of stocks, which is why it they are often referred to as “fear indices” – the more concerned you are that stocks will fall, the more you are willing to pay for insurance.

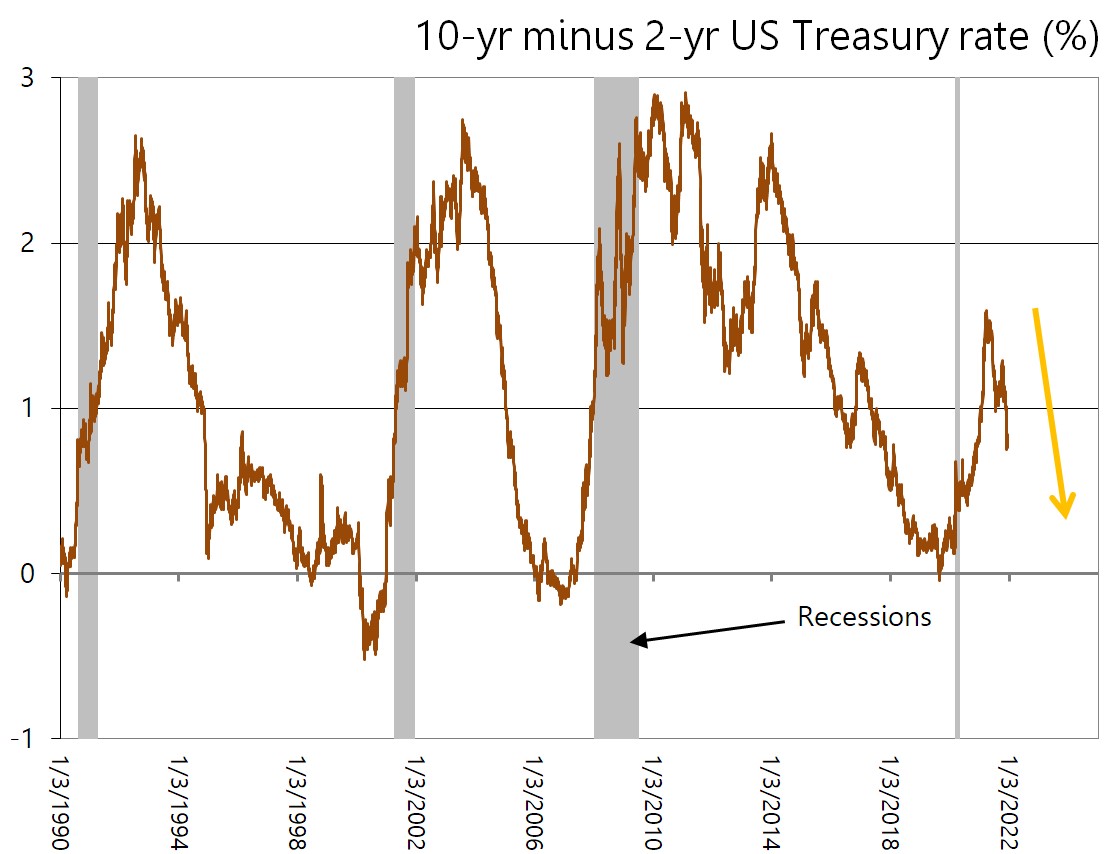

Second, the yield difference between the 10-year and the 2-year U.S. Treasury notes is less than 0.8%, half of what it was in the first quarter after narrowing quickly in the last few weeks. The reason why this is concerning is that this difference reflects the view of market participants about the economic outlook: The narrower it is, the weaker the prospects. The few occasions when it turned negative were followed a few quarters later by recessions. It is still far from being negative, but the rapid decline suggests that the market is quickly becoming convinced that the economy will slow down.

source: Path Financial LLC, Standard and Poors

source: Path Financial LLC, Standard and Poors

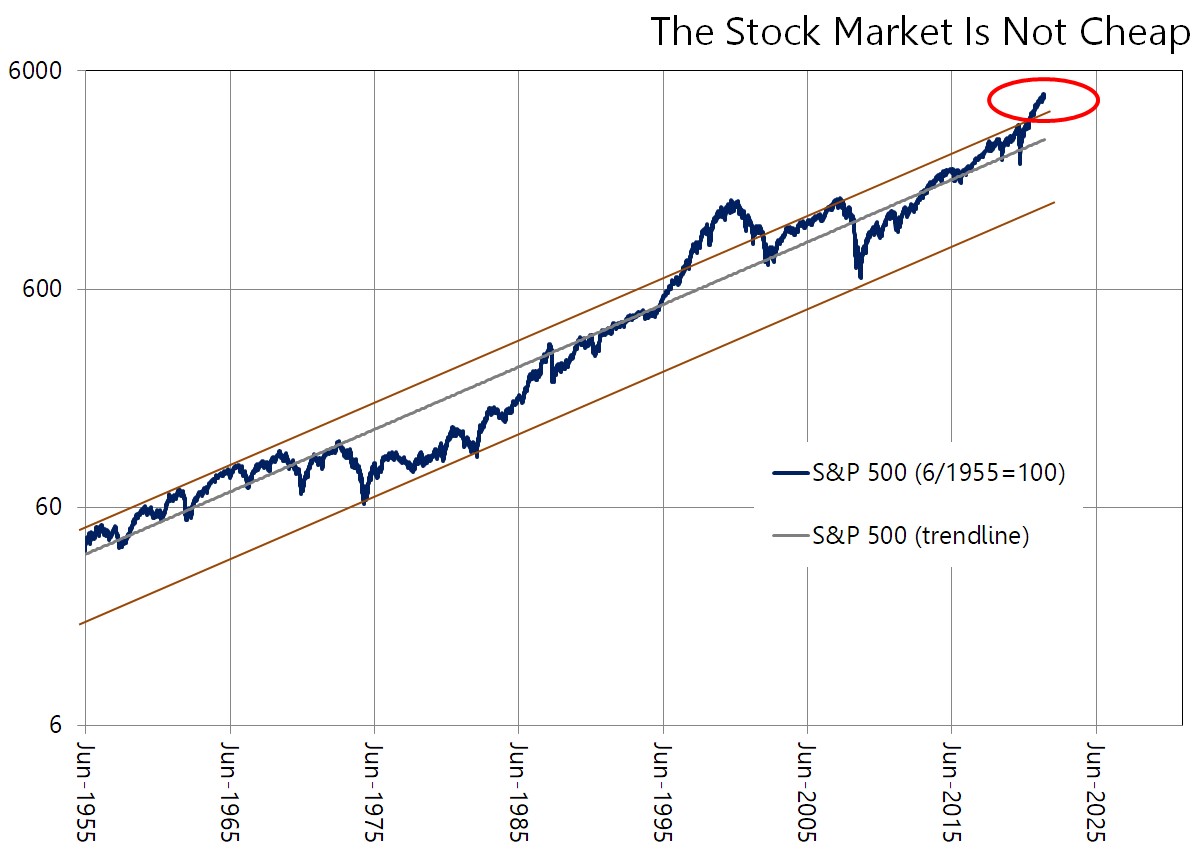

Finally, as

we wrote not long ago, stocks seem expensive. Sometimes this is brushed off as a quirk in the aggregate index (the S&P 500). Because the constituent stocks are weighted by market cap, the reasoning goes, large and high-flying stocks like Amazon, Apple or Microsoft have a disproportional effect on the index value, making the entire market look expensive when in reality that is true of only a handful of stocks.

source: Path Financial LLC, U.S. Federal Reserve

source: Path Financial LLC, U.S. Federal Reserve

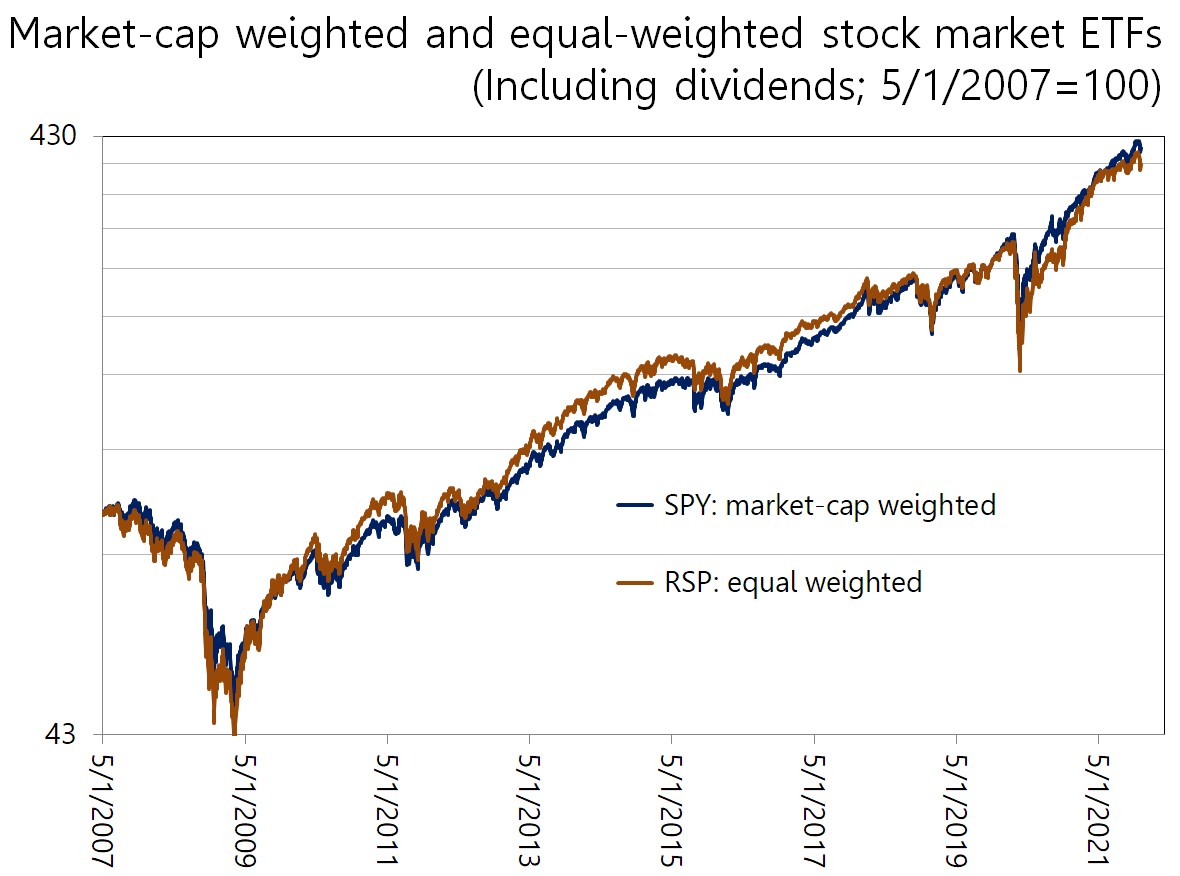

This argument does not really hold up. There is an index that assigns the same weight to every stock, large or small, in the S&P 500. While the market-cap index (the S&P 500) seems marginally ahead of the equal-weight index in recent months, it is hard to argue that the big-stock effect is really at play when the indices are plotted together. Either way you look at it, the equity market is at the top of its historical trend band.

source: Path Financial LLC, Standard and Poors

source: Path Financial LLC, Standard and Poors

While all this is not enough to conclude that stocks are about to crash, there is no doubt that the economy and markets are more fragile, and the short-term outlook far less bright, than only a few months ago. We are still shifting through the aftermath of the pandemic trying to understand its impact on everything. Few, if anyone, predicted the labor shortages, supply disruptions and 180-degree turn from a dovish Fed to a hawkish Fed.

Throw in the mix ballooning global government debt, a resurgence of populism everywhere, renewed geopolitical tensions and much more and it becomes clear that forecasting markets or economic conditions has rarely been this difficult. By definition, this means that much of what happens in the next few quarters is likely to hit investors unprepared. Short-term volatility, therefore, seems inevitable.

Investors who don’t have a long horizon or can’t stomach volatility may be well served by reducing their portfolios’ risk exposure. Stocks have been in bull market for a long time, are still close to their all-time high and the most aggressive stocks were the biggest winners. This seems to be an excellent opportunity to take some profits and explore more defensive, lagging sectors like consumer staples or health care until the outlook becomes clearer.

Of course, this could exact an opportunity cost if markets continue at the same torrid pace it clocked since the pandemic low, so some investors will proceed full-speed ahead for fear of leaving gains on the table. Wall Street long-timers will retort that hogs get fat but pigs get slaughtered.

Questions?

Talk to us.