By Raul Elizalde

This article also appeared on forbes.com

A

recent report by Oxford Economics reveals that their index of supply strains reached a peak in March. The price of commodities, transportation and other inputs remains stubbornly high, helping drive inflation to its worst level in decades.

The Federal Reserve responded by declaring war on inflation and adopting the role of the leading hawk, despite a) having done nothing other than a near-irrelevant 0.25% Fed Funds rate hike and b) knowing full well that it cannot do anything about the supply-chain factors driving prices through the roof.

The difference between the Fed’s actions and rhetoric is stark, but understandable: It is exceedingly difficult to tackle inflation in an economy where the stock market and home values are 30% above pre-pandemic levels, unemployment is at rock bottom, checking accounts are flusher than ever thanks to the lingering effects of many stimulus packages and the public is eager to go on vacation and restaurants. Cooling off an economy doing this well will be hard.

In this environment the Fed has two conceivable ways of approaching inflation. One would be to wait it out if they secretly believe, perhaps reasonably, that the supply chain problems will eventually work themselves out and input prices will come down. Another would be to embark on consumer demand destruction by attacking the ability of businesses to pass their higher costs to consumers. To succeed, they need to make the public spend less by making them feel poorer or more worried about the future. The first one is politically suicidal. The second will require a lot of effort and it may end up tanking the economy.

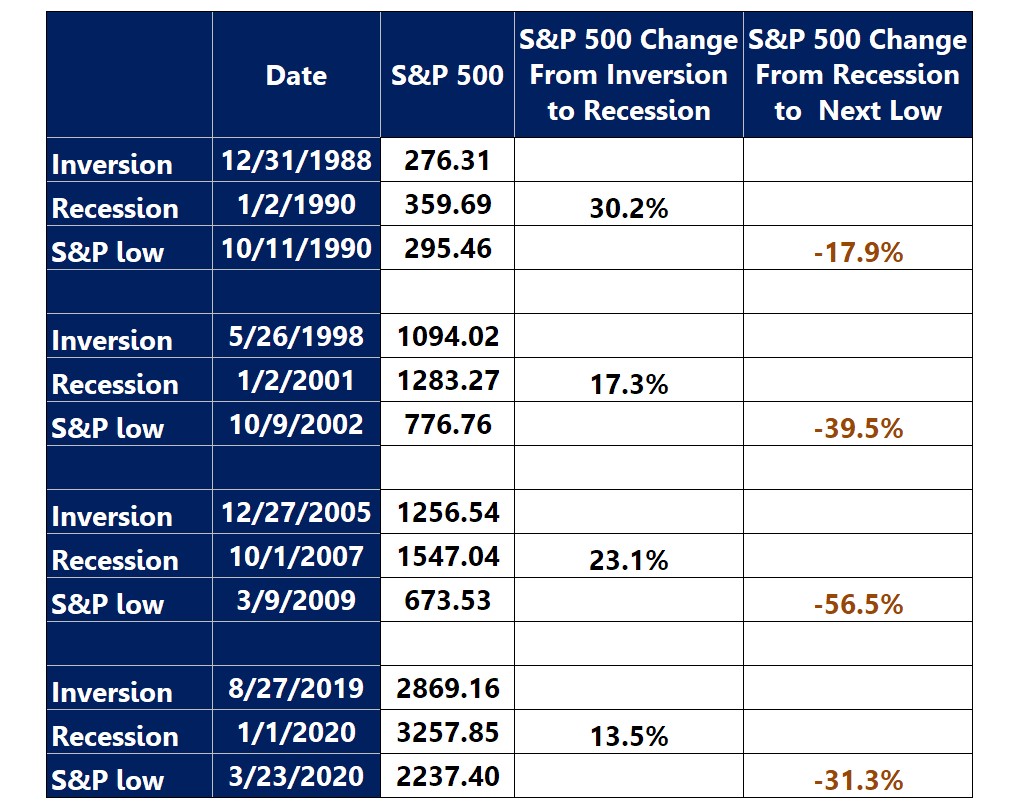

Clearly the bond market believes that the Fed’s jawboning will be backed with action. Interest rates soared, bond prices tumbled and the yield curve inverted, ever so briefly, sending the 2-year Treasury bond rate above the 10-year. This is unusual because longer maturities almost always trade at higher rates, and in the past a recession often followed after the yield curve inverted. But recessions don’t always happen after inversions – although they did the last four times – and when they do, they take many months to arrive.

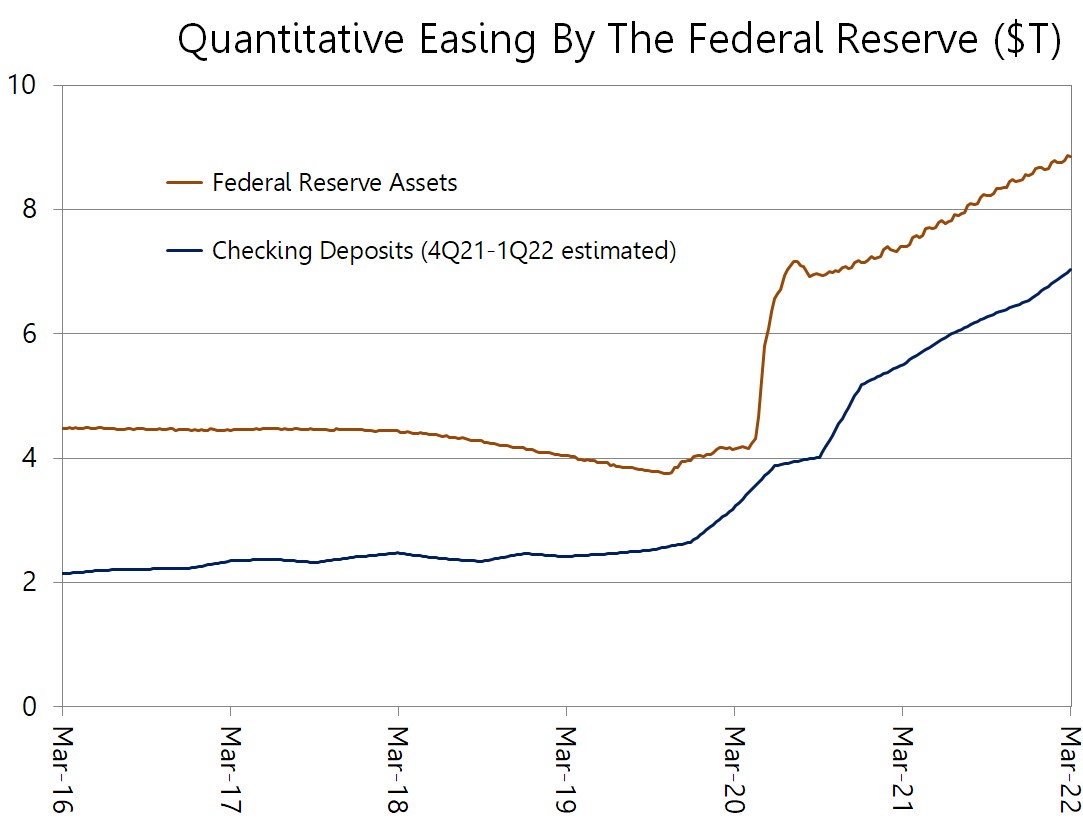

Interest rates are not the only tool the Fed can use: Controlling money supply has been even more important in recent years, especially after rates bottomed out at zero and the Fed couldn’t use them anymore to loosen policy further when needed, not just in the early days of the pandemic but after the 2008 financial crisis.

One way the Fed increases the money supply – i.e. injects money – is by buying bonds. The money is “printed” by crediting a bank’s reserves accounts at the Fed for the value of the bonds the bank purchases on the Fed’s behalf. Since banks can lend multiple times the amount of their reserves, they “create” money and inject it into the system.

In practice, this did not quite happen like the Fed intended as banks did not lend much, for reasons beyond the scope of this post. At any rate, the bonds purchased by the Fed became assets and the credited amount to bank reserves became liabilities, thus increasing the size of the Fed’s balance sheet. This is “Quantitative Easing”, or QE. The opposite – reducing assets by selling bonds or letting them mature without replacement – is Quantitative Tightening, or QT.

The Fed’s balance sheet became bloated with bonds and other instruments to levels inconceivable in the past, and it has not come down by any discernible amount yet. Fed officials just indicated that a decision on the pace of asset reduction will be made in May and it may kick off in June. This does not sound like a Fed in a hurry to tighten.

To be sure, nobody has a clear understanding about how reducing the Fed’s balance sheet could impact the economy. Fed Governor Christopher Waller is quoted in the Wall Street Journal as saying that they “have no economic theory of how large the central bank’s balance sheet should be.” One thing is clear, however: The total amount of money in private checking accounts is now three times larger than before the pandemic, and it is correlated to the size of the Fed’s balance sheet through the interactions between the Fed, the banks and the public.

source: Path Financial LLC, Federal Reserve Bank of St. Louis

source: Path Financial LLC, Federal Reserve Bank of St. Louis

As long as consumers have plenty of cash, higher interest rates will have a limited effect on their spending habits. And if inflation persists, spending may actually increase because prices will be expected to be higher tomorrow than today.

Strong retail sales numbers, indeed, don’t show that the consumer has stepped back in any significant way. This means that QT has to be used aggressively to reduce those cash balances if it has any hope of impacting consumer demand. This will be the easy part. The other factors that keep people spending – a tight job market, the high values of their savings and the pent-up demand from the pandemic days – will be much more difficult to address without creating real pain.

In the absence of any significant action, consumer strength is bound to persist for some time. This could be a strong pillar for the stock market this quarter and possibly next. But these conditions are such an obstacle to the Fed’s demand-destruction mission that, if inflation remains high, the Fed may end up being too late, doing too much and setting the stage for a recession later on. This would be especially true if they are currently buying time, hoping for improving supply conditions in private while talking tough in public.

This outline aligns well with previous pre-recession experiences. The market rallied for a few months or quarters after the yield curve inverted and then was hit hard when the recession arrived.

source: Path Financial LLC

source: Path Financial LLC

If this is what’s going on, the next quarter or two can be particularly treacherous. A resumption of the market rally may turn investors complacent and their guard will come down just when things start to take a bad turn. Of course, the Fed could also succeed in bringing down inflation and pulling off a soft landing. Chances that it will turn out like that are not great.

Questions?

Talk to us.